by Charles Plant | May 18, 2021 | Entrepreneurship

I heard from an entrepreneur I know that a very prominent institutional investor turned down their request for Seed Round funding because the company is pre-revenue. There is no way this company can get to revenue without a reasonably large amount of funding and it made me realize that this is the Catch 22 of Canadian Seed Funding. Now many of you have heard similar statements in the past from VCs, but I’ve been thinking about this because of the problem it creates for companies.

When companies hear that VCs won’t invest pre-revenue they translate this to mean that when you have some revenue, funding may be available so whatever you do, it should be focussed on getting a product launched so you can get some revenue. What will an entrepreneur do in a situation like this? They will prioritize product development over customer discovery. With limited funding from pre-seed money there typically isn’t enough money to do both customer discovery/product marketing and product development. So, they put almost all their money in product development and little in product marketing.

As a result, companies that I meet typically have done very little and in some cases no customer discovery before they bring a product to market. They have also not typically spent much time on market sizing, competitor discovery, customer market research and a whole host of pre-revenue activities. And why are they doing this? It’s because this is what investors are telling them to do when they inform them that they won’t invest until they have some revenue.

The end result is companies that rush products to market, find a customer if they are lucky, raise some funding once they have revenue and then they have money to do customer discovery. But at this stage the customer discovery often tells them that the market they thought might be there, isn’t there for the same product they developed. So, they go back to the drawing board and rejig the product so that it meets the market needs that they discovered too late.

Now they are using Seed funding for customer discovery and to recreate their product, frequently having to pivot into something entirely different. But having to relaunch or pivot slows down growth so when they come to look for a Series A Round, their growth is low and investors are not interested. Now they are dead in the water. And why is this? It is often because they couldn’t raise funds to do proper customer discovery before they launch.

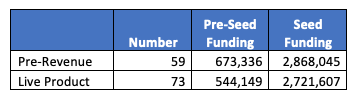

I wanted to look at what stage a company needs to be in to get financing in the US because rumours abound that US venture capitalists will fund a company earlier than a Canadian VC will. To do that research I looked at 132 companies that had received Seed Capital In one month, checking that same month as to whether they had a live product available to ship or did not have a live product and were thus pre-revenue. Here are the stats.

What this implies is that 45% of the companies in this test were able to get seed capital financing without revenue. Oddly enough, these companies had a higher level of pre-seed funding (averaging $673 thousand) and the Seed funding they did get was marginally higher ($2.9 million). In the US then, being pre-revenue isn’t a big impediment to getting funding and a firm like the one I was talking to wouldn’t hear the pre-revenue response so often.

I understand that there will always be some seed stage funders who want to see revenue before considering funding but I think this is a typically Canadian problem. The problem is the small size of our market. With fewer firms seeking funding, a Canadian VC that funds entirely or mostly Canadian companies will see companies in a variety of markets and will not be able to specialize and get to know particular markets in the same depth as US VCs who see more companies will. With less market knowledge, Canadian VCs will have to rely on other signals as to whether a company has potential. The easiest route is to rely on the market thus the requirement that a company have revenue before a VC will consider investing.

This results in the Catch 22 of Canadian seed funding that requires that a company have revenue before investing. It’s sad for the companies that need more money to launch a product. What are they to do? What they have to do is go down to the US to get funding. Find a US or foreign VC which will support them pre-revenue.

This blog is part of what we discuss in a workshop series hosted by Communitech. You can find out more about it by clicking here. If you want to receive more blogs like this, you can subscribe by filling in the space on the right.

by Charles Plant | May 11, 2021 | Entrepreneurship

A number of years ago I had one of those AhHa! moments that one has when one is fiddling around doing research. Basically, I discovered the surprising way initial funding drives success. I was playing around with Crunchbase, looking at the 2,429 healthcare and computer technology businesses launched in 2008 in Canada, the US, the UK, France, and Germany to see how they had developed. Since founding 983 had obtained capital of over $100,000 to fuel their growth.

I was trying to figure out how funding fuelled growth; whether if there are patterns that could indicate the optimal amount of funding, round size, the number of rounds, when to raise capital etc. Basically, I was out fishing to see if I could catch anything close to a trend. I narrowed the research down to all software companies worldwide which had raised more than $1 million cumulatively to make results comparable. That left me with 640 companies.

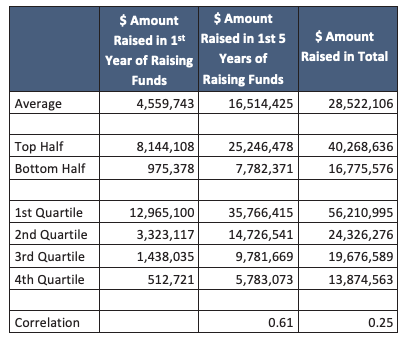

One of the tests I did was to see if there is any correlation between how much money a company raises the first time it raises funds and how they do in the long run. I stratified the results from the 640 companies into 4 quartiles, depending on how much they had raised in their first year of raising funds. The following exhibit shows the data I discovered.

These results are very clear: those firms that raised the highest amounts the first time they raised funds subsequently raised far more than firms who raised less capital in their first year of fund raising. The relationship is particularly strong in the first five years of fundraising, with a correlation of .61, showing that there is a definite advantage to raising more money the first time you raise it. This relationship is still true over the long run, though not as strong.

The logic behind this is self-evident when you look at the effect of capital on revenue. The more capital you raise, the more employees you can hire and the more revenue you can drive. Raising more money in your first year of fund raising enables you to grow faster (given a large market) and the faster you grow, the more likely you’ll be to attract investment in your next round, thus initiating an accelerated growth curve.

So, for me, the surprising way initial funding drives success is as follows:

The more money you raise the faster you’ll grow

And the faster you grow, the more money you’ll raise.

Maybe this shouldn’t have been surprising but given the way many entrepreneurs and investors talk about capital efficiency, it runs counter to common wisdom. If you’re planning on raising capital this relationship shows that it doesn’t pay to be conservative, it pays to be very aggressive, raising as much money as you can as long as you can produce results.

This blog is part of what we discuss in a workshop series hosted by Communitech. You can find out more about it by clicking here. If you want to receive more blogs like this, you can subscribe by filling in the space on the right.

by Charles Plant | May 5, 2021 | Entrepreneurship

We were sitting on one of those lovely Zoom calls the other day at The Happenin Company, debating about how much seed capital we should raise. Of course the simple answer is raise as much money as you need to get to a Series A round in 18 to 24 months. But it helps to know how much others are raising to understand if you are in the same ballpark. I figured I could do a bit of research and at least see if there is any way to use data to answer the question. And I figured there might be a few other people out there who might appreciate an answer so I created this blog. It is the first in what will be a series that will look at different issues in raising seed capital.

To start to put a perspective on this issue, I went back to some research I did a year ago that looked at fundraising patterns of over 500 firms in the US and Canada in late 2019. I only looked at firms that had raised over $1 million. Of the 500 or so firms, 138 of them had raised a Seed round so was included in this analysis. First up are some big stats.

The Data

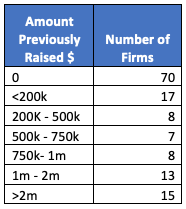

The average amount raised by these firms was $2.8 million ($US) and the median raise was $2.3 million. In this sample, the biggest raise was just under $10 million. Looking at the distribution of firms by how much they raised reveals the following:

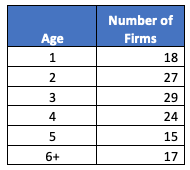

Next up in data is how old these firms are and there is no pattern to age. Firms range from brand new, under a year old to several at 7 and 8 years old and even one at 13.

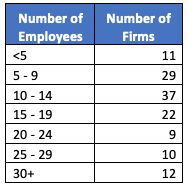

One key determinant of how much to raise is how many employees you already have. To figure this out we looked at LinkedIn. While it isn’t totally accurate, we’ve found from past research that it is directionally correct. We’ll get to this relationship in the last exhibit but meanwhile, here is the data on the distribution of firms by size in employees.

Another key determinant we found was how much a firm had raised previously, perhaps from an accelerator or a pre-seed round. We’ll get to that relationship in a second but here are the stats on previous raises:

Finally Answering the Question

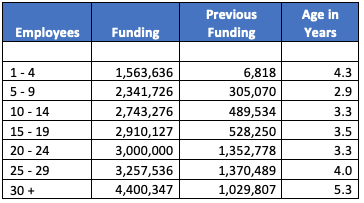

Finally we can put this all together in a picture for you. Here are the funding stats broken down into averages based upon how big a firm is in number of employees.

Every now and then, research really works out for you and this was one of those times. There appears to be a distinct relationship between how big a firm is when it raises money and how much money they raise in a Seed round. It also flows that this relationship extends to how much it has previously raised before doing a Seed round. And this makes sense. As you’re out trying to build a business you have a choice of raising pre-seed money to grow before going to raise a Seed round. The more you raise before the seed round, the farther you can get thus the bigger that you’ll be and the more you’ll raise in that seed round.

So if you’re trying to answer the question of how much seed capital you should raise, looking at the chart will give you a good idea of how to answer it. It will also help you evaluate whether you should raise a pre-seed round and build the firm up farther before raising a seed round.

This blog is part of what we discuss in a workshop series hosted by Communitech. You can find out more about it by clicking here. If you want to receive more blogs like this, you can subscribe by filling in the space on the right.

by Charles Plant | Mar 30, 2021 | Entrepreneurship

We finally got around to launching the Narwhal List 2021. 2020 was another remarkable year for Canadian Narwhals. In particular, four companies from last year’s list went public. (Nuvei, Chinook Therapeutics, Repare Therapeutics, and Fusion Pharmaceuticals.) Five were sold (Element AI, Verafin, North, Fiix, and Northern Biologics.) Of particular note, Verafin, a 17 year old company from St John’s was sold for $2.75 billion. (All Amounts $US)

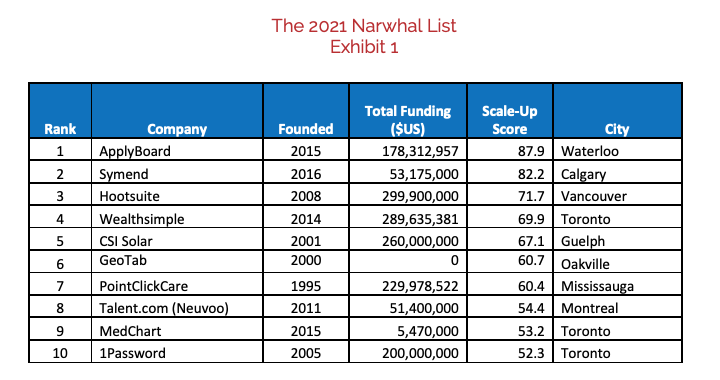

Twenty five companies on the 2021 list raised a total of over $1 billion with the largest raise of the year going to CSI Solar in Guelph which raised $260 million.

Canada now has three Unicorns with PointClickCare finally being recognized as such with a valuation of $4 billion. Applyboard also joins Coveo on the list this year with a valuation of $1.5 billion

This year we have enhanced the scoring system to be able to include firms that are scaling successfully by bootstrapping. What we have created is a Scale-Up Score which reflects the success a firm is having scaling their business. This is explained further in this document. Exhibit 1 features the ten leading Canadian Narwhals. The full list is published here:

The Narwhal List 2021 V5

As would be expected, the greatest number of companies on the list is from Toronto with substantial numbers coming from Montreal and Vancouver as well.

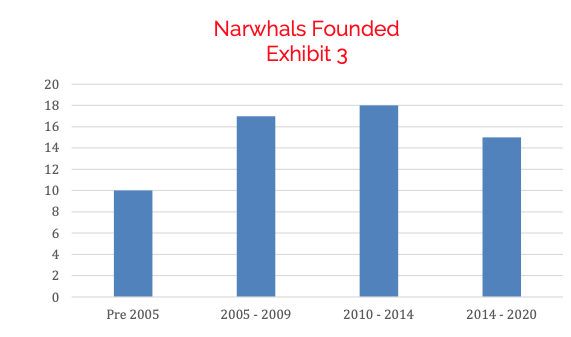

In terms of when these companies were founded, the average year of founding is 2008 with more than half founded since then.

For a white paper with more details on the Narwhal List 2021 click here.

by Charles Plant | May 30, 2020 | Entrepreneurship

Are you wondering about what to do about scaling up in a recession? We are now nearly two months into a combined health and economic crisis. Many companies will have had a chance to address cash flow and strategic issues. Are you ready to examine your cash flow and strategic issues? Do you need a structured approach? Here is some guidance to help you make the right decisions about how to proceed.

For solution providers who are starting or scaling and require substantial venture capital investments to be able to grow, capital may be restricted for some time. During this crisis, venture capitalists are likely to invest in fewer firms, offering lower dollar amounts and for lower valuations. Startups and scaleups that rely on capital infusions will need to conserve cash. The question: How to do that? Here is one strategy to conserve cash:

- Determine whether the markets for your products are the same or have changed and adjust plans accordingly.

- If there are no opportunities in your current market, you will need to pivot.

- If a pivot is not necessary, focus on the market segment with the best potential, instead of the entire market.

- Use this time to concentrate your R&D efforts on improving product differentiation in those markets with the highest potential.

Whether you need to slow down the growth in spending or actually reduce headcount or cut back on marketing communications spending, a strategy of focusing on the highest potential market segments will conserve cash, optimize growth and produce a plan that will be supported by existing and prospective investors. This should be done with a view to focusing on value for customers to drive growth and how this translates to value for investors.

For a white paper on Scaling up in a Recession, click here.

by Charles Plant | Jan 30, 2020 | Entrepreneurship

The Narwhal List 2020 – 2019 was another remarkable year for Canadian Narwhals. In particular, there were 9 financings of Narwhals that exceeded $100 million (all amounts in $US). Two of these financings were in healthtech and 7 in computer technology. Of particular note were deals that provided $388 million to Verafin in St John’s, $270 million to Nuvei out of Montreal, $250 million to Clio from Vancouver and $200 million to Toronto’s 1 Password. It is interesting that all of these companies are more than 10 years old and none had previously made the Narwhal List cut-off.

Several prominent companies graduated from the list this year. Lightspeed POS had an IPO, Bluerock was acquired by Bayer, and Wealthsimple has been classified as acquired as its largest investor now owns more than 50% of the company.

While Kik Interactive was removed from the list of Unicorns maintained by CBInsights, two new Canadian companies made the list. These were Nuvei with a valuation of $2 billion and Coveo with a valuation of $1.1 billion.

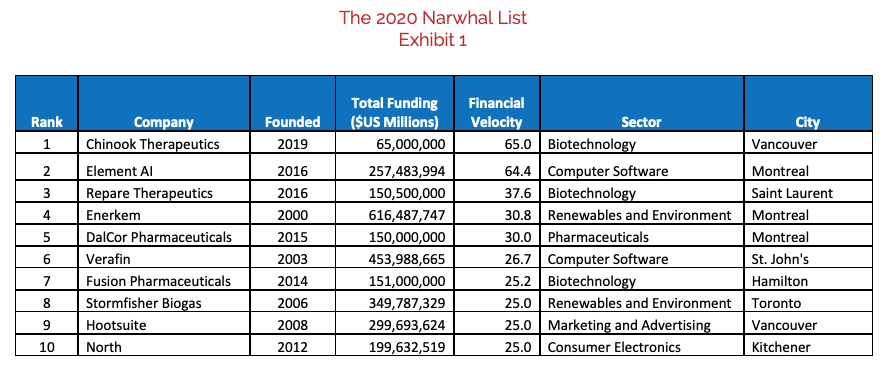

For the first time, we have expanded the list by 10 companies to include cleantech ventures. Exhibit 1 features the ten leading Canadian Narwhals.

The Narwhal List 2020 V5As would be expected, the greatest number of companies on the list is from Toronto with substantial numbers coming from Montreal and Vancouver as well.

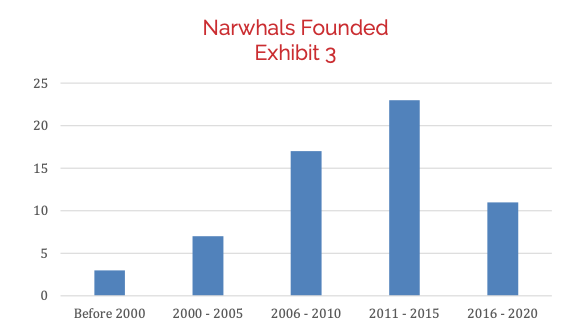

In terms of when these companies were founded, the average year of founding is 2010 with more than half founded since then.

For more information on the Narwhal List 2020, please click here.